What Is the Time Value of Money?

The Time Value of Money (TVM) is the principle that a sum of money available today is worth more than the identical sum available at a future date, because money held today can be invested to earn a return over time. It is one of the foundational ideas in all of finance — from personal savings and home loans to corporate investment analysis and pension fund management.

The concept sounds simple but it has powerful, far-reaching consequences. It means that every financial decision involving different time periods — borrowing, investing, saving, comparing loan offers, deciding when to retire — needs to adjust for the time value of money to make an apples-to-apples comparison. That is exactly what the TVM Calculator does.

Why Money Has a Time Value

There are three distinct reasons money available today is worth more than the same amount later:

- Investment opportunity: money in hand today can be put to work immediately — in a savings account, index fund, or business — and begin earning a return. A dollar received a year from now misses that year of growth entirely.

- Inflation: in most economies, prices rise over time. $100 today will buy more goods and services than $100 will buy one year from now, because the purchasing power of money erodes gradually with inflation.

- Risk: there is always some uncertainty that a promised future payment will actually arrive. A payment in hand today carries zero collection risk; a future payment always carries some, even if very small.

These three forces — opportunity cost, inflation, and risk — combine to mean that any rational person or institution should require a future payment to be larger than a present payment to view them as equivalent. That "extra" amount is what interest represents.

Present Value (PV) — What Is a Future Sum Worth Today?

Present Value is the current worth of a future cash flow or series of cash flows, calculated by discounting those future amounts back to today at a chosen interest (discount) rate.

The core question PV answers: "How much money do I need right now to grow to a certain amount in the future?" You are essentially running the clock backwards — instead of multiplying by interest to go forward in time, you divide to come back.

The basic formula for a single lump sum is:

Verified example: you want $10,000 for your child's college education in 10 years. Your savings account earns 6% per year, compounded annually. How much do you need to deposit today?

A deposit of just $5,584 today grows to $10,000 in ten years at 6%. The TVM calculator's PV solve does this instantly for any combination of values — including when there are regular payments alongside the lump sum.

Future Value (FV) — How Much Will My Money Grow?

Future Value is the amount a sum of money (or a series of payments) will grow to at a given interest rate over a given number of periods.

The question FV answers: "If I invest money today, what will it be worth later?"

The basic formula for a single lump sum is:

Verified example: investing $2,000 today at 7% annual return for 30 years:

FV = $2,000 × (1.07)30 = $2,000 × 7.6123 = $15,224.51

A single $2,000 investment grows to over $15,000 in 30 years — more than 7× the original amount — without adding a single extra dollar. This is the power of compounding (explained below).

Compounding — The Engine of Growth

Compounding means earning interest on your interest, not just on the original amount. Each period, the new interest is added to the balance, so the next period's interest is calculated on a larger base — creating an accelerating, exponential curve of growth.

This is easiest to see by comparing compound interest to simple interest over time. Simple interest pays the same fixed dollar amount each period (no snowball effect). Compound interest reinvests each period's earnings, so the snowball gets bigger every year.

Both lines start at $2,000. After 30 years the compound investor has $15,225 vs the simple-interest investor's $6,200 — a gap of over $9,000 from the same starting amount and the same rate.

Compounding frequency matters too. The more often interest is compounded within a year, the more you earn. Monthly compounding produces a slightly higher result than annual compounding at the same stated rate. The TVM calculator handles any compounding frequency via the C/Y (compoundings per year) setting.

| Compounding Frequency | C/Y Setting | Effective Annual Rate (at 6% nominal) |

|---|---|---|

| Annual | 1 | 6.000% |

| Semi-Annual | 2 | 6.090% |

| Quarterly | 4 | 6.136% |

| Monthly | 12 | 6.168% |

| Daily | 365 | 6.183% |

Interest Rate (I/Y) — The Speed of Growth

The interest rate (labeled I/Y in the TVM calculator, meaning "interest per year") is the annual rate at which money grows when invested, or the annual rate charged on a loan. It is the single most powerful variable in TVM: small differences in rate, compounded over decades, produce enormous differences in outcome.

The TVM calculator solves for I/Y using a numerical method called Newton-Raphson iteration, because the interest rate cannot be isolated algebraically from the full TVM equation the way the other four variables can. When you click SOLVE next to I/Y, the calculator runs this iterative process automatically — you simply provide the other four values.

Real-world tip: when comparing investment accounts or loan offers, always ask for the effective annual rate (EAR), not just the nominal rate — they differ whenever compounding is more frequent than annual. Our calculator's C/Y setting lets you convert between them transparently.

Number of Periods (N) — Time Is Your Biggest Lever

N is the total number of payment or compounding periods — for a 30-year monthly mortgage, N = 360; for a 5-year annual investment, N = 5. It seems like a simple input, but time is actually the single most powerful lever in all of TVM. The compounding chart above illustrates why: the exponential curve accelerates in the later years, meaning an investor who starts 10 years earlier and contributes less total money can still end up wealthier than one who starts later but contributes more.

When the TVM calculator solves for N, the result is often a decimal (e.g., 314.7 months). That's normal — it means the loan or savings goal doesn't divide evenly into whole periods at that exact payment. Round up to a whole number to get a practical payoff date.

Annuities — Regular Equal Payments

An annuity is a series of equal payments made at regular intervals. Examples include monthly mortgage payments, car loan instalments, regular retirement contributions, and pension disbursements.

Ordinary Annuity (END mode)

Payments occur at the end of each period. This is the standard for most loans, mortgages, and retirement savings plans — the payment is due after the period's interest has accrued. It is the default setting (END) in the TVM calculator.

Annuity Due (BGN mode)

Payments occur at the start of each period. This is common for rent and most lease agreements — you pay at the beginning of each month. Because each payment is made one period earlier, it has more time to grow (for savers) or accrues interest differently (for borrowers). Switch to BGN mode in the calculator for any lease or rent scenario.

| Feature | Ordinary Annuity (END) | Annuity Due (BGN) |

|---|---|---|

| Payment timing | End of each period | Start of each period |

| Common uses | Mortgages, car loans, bonds | Rent, leases, insurance premiums |

| For savers | Standard retirement contributions | Higher FV — each payment earns one extra period of interest |

| For borrowers | Interest accrues before payment | Payment made before interest accrues that period |

| TVM calculator setting | END (default) | BGN |

Perpetuities — Payments That Last Forever

A perpetuity is an annuity that makes equal payments at regular intervals indefinitely — with no end date. Real-world examples include certain government bonds (UK Consols), preferred stock dividends, and endowment funds designed to pay out forever.

Because the payments go on forever, the formula simplifies elegantly — the infinite series converges to a finite present value:

Verified example: a trust fund is set up to pay $5,000 per year forever. At a 5% discount rate, the present value (how much you need to fund it) is:

A perpetuity is a good mental model for understanding why interest rates and asset prices move in opposite directions: if the rate doubles, the present value of any fixed-payment stream halves — which is why bond prices fall when interest rates rise.

The Five TVM Variables — How They Work Together

The TVM calculator ties all five variables (N, I/Y, PV, PMT, FV) into a single master equation. Give it any four and it solves the fifth — in the same way a basic financial calculator used in finance courses works:

where r is the interest rate per payment period (converted from I/Y, P/Y and C/Y), and F is 1 for BGN mode or 0 for END mode. The sign convention is: inflows positive, outflows negative.

Worked Examples for Every Audience

For Students — Saving for a Goal

You want to have $20,000 saved for a gap year trip when you finish college in 5 years. A high-yield savings account currently pays 5% per year, compounded monthly. You have nothing saved yet. How much do you need to put away each month?

- N = 60 (5 × 12), I/Y = 5, PV = 0, FV = 20,000, solve PMT

- Result: PMT ≈ −$294.13/month

About $294 a month for five years gets you to $20,000. Notice PV = 0 because you are starting from scratch, and FV is positive because the $20,000 is money you will receive from the account.

For Working Professionals — Retirement Planning

You are 35 years old with $25,000 already saved, and you want to retire at 65 with $1,000,000. You expect an 8% annual return, compounded monthly. How much do you need to contribute each month?

- N = 360, I/Y = 8, PV = −25,000 (money already invested = outflow you've made), FV = 1,000,000, solve PMT

- Result: PMT ≈ −$670.98/month

Just under $671 a month, on top of the $25,000 head start, reaches $1,000,000 in 30 years at 8%. If you had no head start, the PMT required would be higher — which illustrates concretely why starting early matters so much.

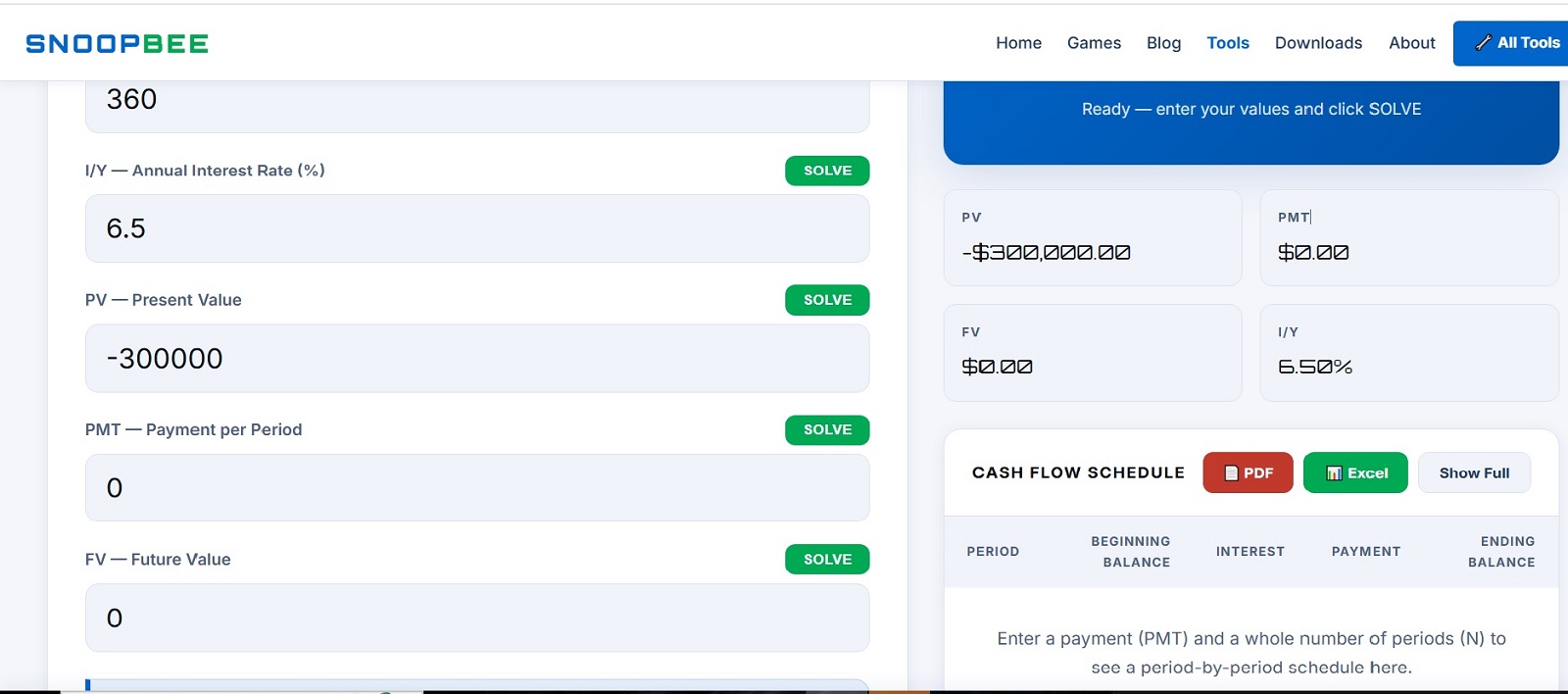

For Home Buyers — Comparing Loan Costs

A $300,000 home loan: lender A offers 30 years at 6.5%; lender B offers 15 years at 6.0%. Here are the verified numbers:

| Feature | 30yr @ 6.5% | 15yr @ 6.0% |

|---|---|---|

| Monthly Payment | $1,896.20 | $2,531.57 |

| Total Paid | $682,633 | $455,683 |

| Total Interest | $382,633 | $155,683 |

| Interest Saved (15yr vs 30yr) | $226,950 | |

The 15-year loan costs $635 more per month but saves $226,950 in total interest. TVM makes this tradeoff completely transparent — use the TVM calculator's PMT solve, then compare the totals by multiplying payment × N.

For Retirees — Lump Sum vs Annuity

You've inherited an estate and are offered a choice: receive $500,000 today, or $40,000 per year for 20 years. Which is worth more?

This depends entirely on what discount rate you apply — i.e., what return you could reasonably earn on $500,000 if you took it today. Here are the verified present values of the $40,000/year stream at several rates:

| Discount Rate Assumed | PV of $40,000/yr for 20yr | vs $500,000 lump sum |

|---|---|---|

| 4% | $543,613 | Annuity worth more |

| 6% | $458,797 | Lump sum worth more |

| 8% | $392,726 | Lump sum worth more |

If you can invest the lump sum at 6% or better, take the $500,000. If your safe withdrawal rate is closer to 4%, the annuity is actually worth more in present-value terms. The TVM calculator's PV solve computes any of these rows in seconds.

Common Mistakes to Avoid

- Starting too late. The compounding chart above shows the explosive growth in the final decade. Missing those years is costly and irreversible — time is the one input you can never buy back.

- Ignoring compounding frequency. "6% interest" means different things depending on whether it compounds annually, monthly, or daily. Always check C/Y in the calculator and compare effective annual rates.

- Mixing up sign conventions. If PV and PMT have the same sign in the calculator, you have described an impossible cash flow and the answer will be wrong or nonsensical. Outflows must be negative, inflows positive (or choose the opposite convention consistently).

- Comparing nominal rates across different compounding periods. A 6% monthly-compounding rate is not the same as a 6% annual rate — use the effective annual rate (EAR) for any like-for-like comparison.

- Confusing END and BGN. A lease payment is typically BGN — entering it as END will give you a wrong payment amount. Always check which mode applies before solving.

Tips for Every Stage of Life

K–12 Students

The most important TVM lesson you can learn right now costs nothing: time is your greatest financial asset. A 16-year-old who saves $50 a month starting today will have more wealth at 65 than a 30-year-old who saves $200 a month starting then, at the same rate of return. Use the FV solve in the calculator, set N to how many months until you turn 65, and watch what even tiny contributions do over 50 years. The number will surprise you.

College Students & Early Career

You are making loan decisions right now. Use the PMT solve to see your actual monthly payment before you sign anything. Use the PV solve to understand the real cost of "buy now, pay later" offers — zero-interest promotions often revert to high rates if not paid in full. And start retirement contributions as early as possible, even tiny ones — the compounding clock starts the moment you make your first contribution.

Working Professionals

You are likely managing the most complex financial decisions of your life — mortgages, car loans, investment accounts, possibly a business. Use the N solve to find out when you'd pay off a loan if you made extra principal payments. Use the I/Y solve to compute the true annual return on an investment you're evaluating. Before refinancing a mortgage, model both scenarios and compare the total interest paid, not just the monthly payment.

Retirees

TVM is essential for understanding whether your savings will last and at what rate you can safely withdraw. Use the PMT solve with PV as your current nest egg, FV as your desired remaining balance (or zero if you plan to exhaust savings), N as your planned years of retirement, and I/Y as your expected return — the result is your sustainable monthly draw. Model several scenarios with different assumed returns to understand how sensitive your plan is to market performance.

Put These Concepts to Work

Open the TVM Calculator →This article is for general educational purposes only and is not financial advice. All figures are illustrative examples calculated from the standard TVM formula and independently verified. Your actual rates, returns, and loan terms will vary. Consult a licensed financial advisor for decisions based on your individual circumstances.

💬 Reader Questions & Feedback

Ask a question about TVM, share a worked example, or leave feedback on this guide. (Max 200 words)