What Is a Mortgage? (Quick Definition)

A mortgage is a loan used to buy real estate, where the property itself acts as collateral. If the borrower stops making payments, the lender has the legal right to foreclose — take possession of the property and sell it — to recover the outstanding balance. In exchange for that security, mortgage lenders typically offer lower interest rates and much longer repayment terms (commonly 15 or 30 years) than unsecured loans. A mortgage has three core ingredients that determine the payment: the principal (how much you borrow, usually the home price minus your down payment), the interest rate (the lender's charge for lending the money, expressed as an annual percentage), and the term (how many years you have to repay it). Everything else in this guide — PITI, amortization schedules, extra payments, refinancing — builds on top of this basic three-part structure.

What Is Amortization? (Quick Definition)

Amortization is the process of paying off a loan over time through a series of fixed, regular payments. Each payment is split into two parts: the interest charged on whatever balance is still outstanding, and the principal, which reduces that balance. Because interest is calculated on a shrinking balance, the split between the two changes every month — early payments are mostly interest, later payments are mostly principal — until the loan reaches exactly zero on its final scheduled payment. The month-by-month record of this split is called an amortization schedule, and it's the backbone of every mortgage calculator, including the one on this site.

Why Understanding Your Mortgage Matters

Buying a home is one of the most significant financial decisions most people ever make. For most homeowners, a mortgage is the largest debt they will carry in their lifetime. A typical 30-year mortgage on a $350,000 loan at 6.5% results in paying over $446,000 in interest alone — more than the original loan amount. That's not a scare statistic; it's simple arithmetic, and you can verify it yourself in the table below. Understanding exactly how your monthly payment is built, and how small changes ripple through the entire loan, can save you tens or even hundreds of thousands of dollars.

This guide walks through every concept used in our Global Mortgage Calculator in plain language — whether you're a student learning the basics of personal finance, a first-time buyer comparing offers, or simply someone who wants to know exactly where their money goes every month.

What makes mortgages confusing isn't the math itself — it's that a single number, your "monthly payment," is actually the sum of several independent moving parts: the loan formula, your local property tax rate, your insurance premium, possibly mortgage insurance, and possibly an HOA fee. Each of these can change independently of the others. A lender quoting you a "low rate" tells you almost nothing about your real monthly cost until you add in the rest. That's the entire reason a proper mortgage calculator exists — to combine every component into one accurate, true monthly number, and to let you see exactly how that number changes over the decades of the loan.

The Basic Mortgage Formula

Every fixed-rate mortgage calculator, including this one, is built around a single formula:

- M = Monthly principal & interest payment

- P = Loan amount (home price minus down payment)

- r = Monthly interest rate (annual rate ÷ 12)

- n = Total number of monthly payments (loan term in years × 12)

This is the same formula banks and professional lenders use worldwide. One country-specific wrinkle: Canadian mortgages compound semi-annually by law, so the calculator converts the semi-annual rate into an equivalent monthly rate before applying this same formula — the math underneath is identical, just adjusted for that legal requirement.

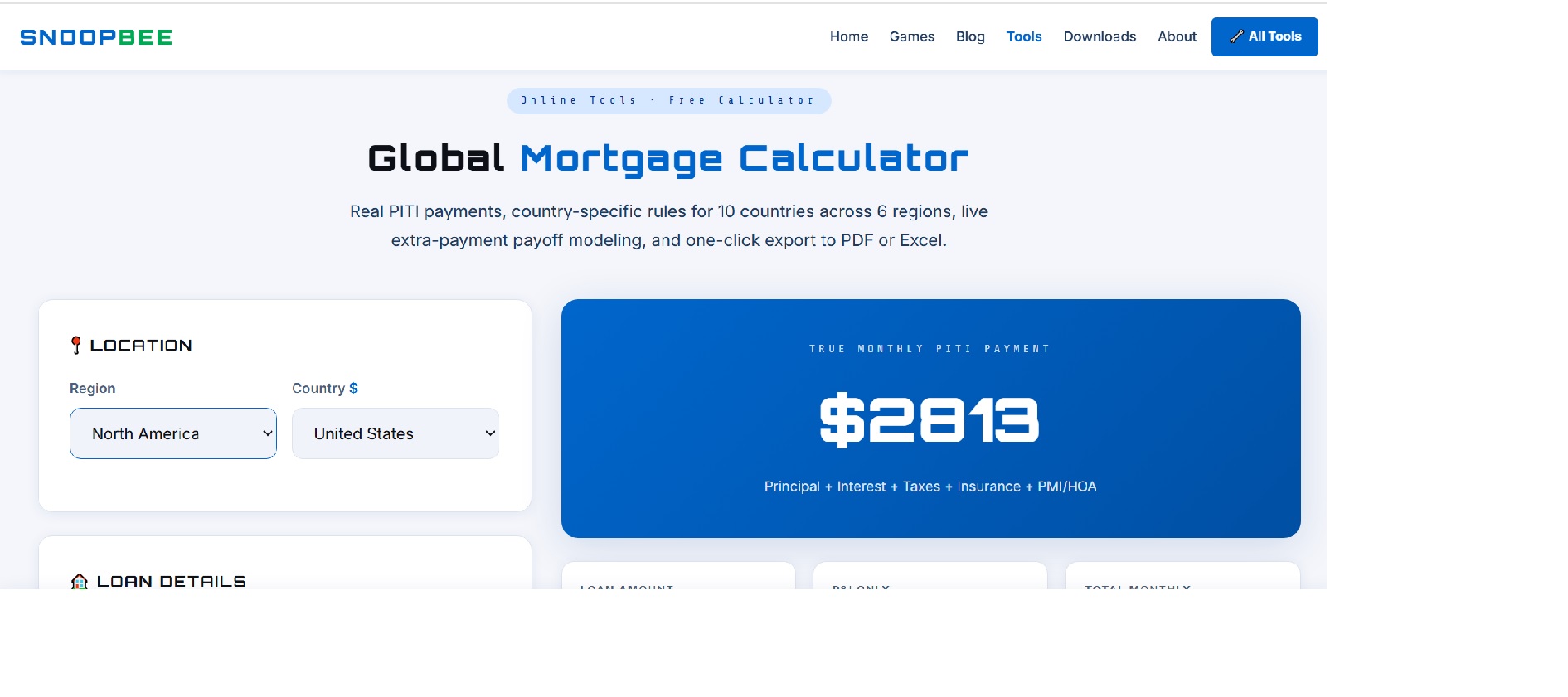

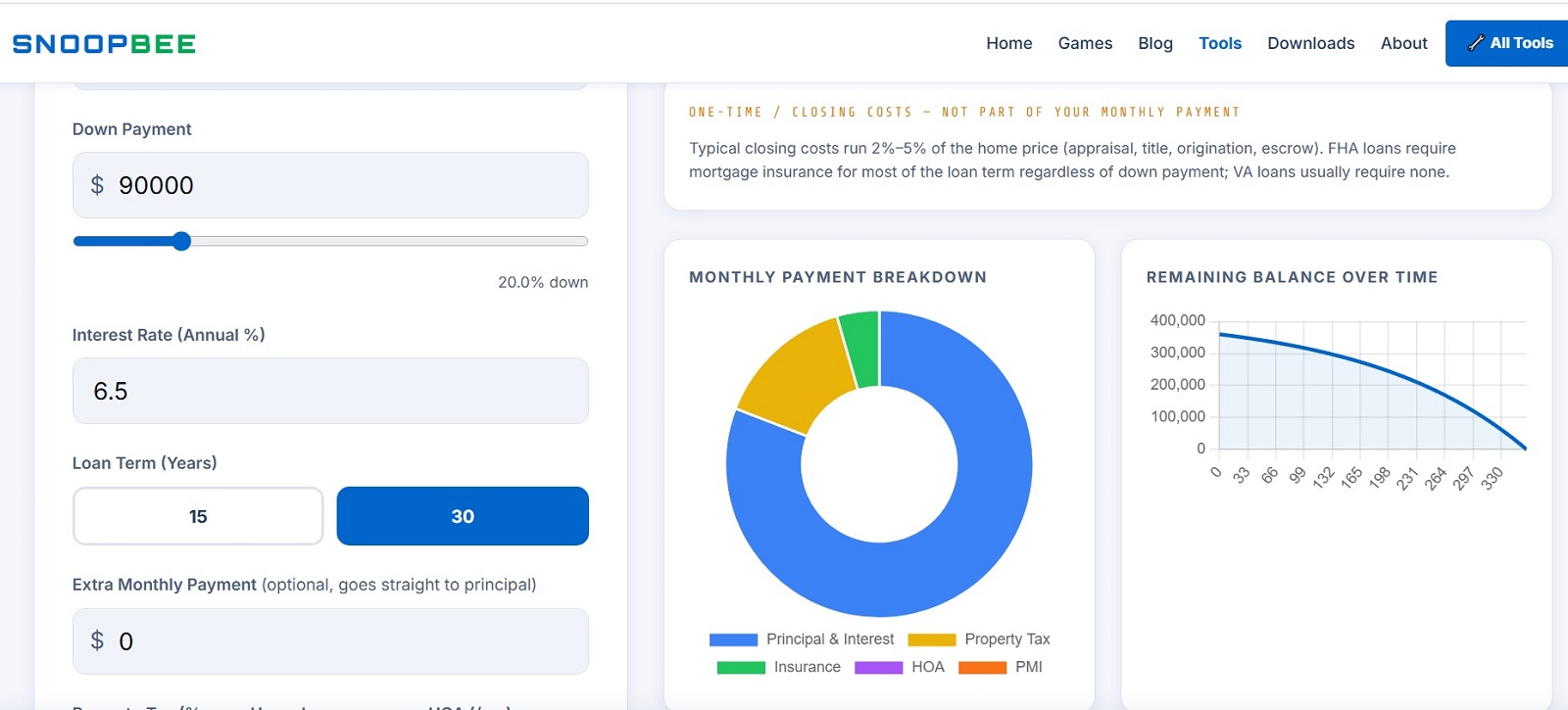

What Is PITI? Your True Monthly Cost

When people say "my mortgage payment," they often mean only principal and interest. But your real, all-in monthly housing cost is usually higher. Lenders and experienced homeowners use the acronym PITI:

- P — Principal (paying down the loan balance)

- I — Interest (the cost of borrowing the money)

- T — Property Taxes (paid to your local government, often collected monthly into an escrow account)

- I — Homeowners Insurance

On top of PITI, two more costs frequently apply: HOA fees (if the property is in a homeowners association) and PMI — Private Mortgage Insurance — which conventional US lenders require once your down payment is below 20% (loan-to-value above 80%). PMI protects the lender, not you, but it's a real monthly cost you need to budget for. Our calculator adds all of these together so the number you see is your actual out-of-pocket monthly cost, not just the loan math.

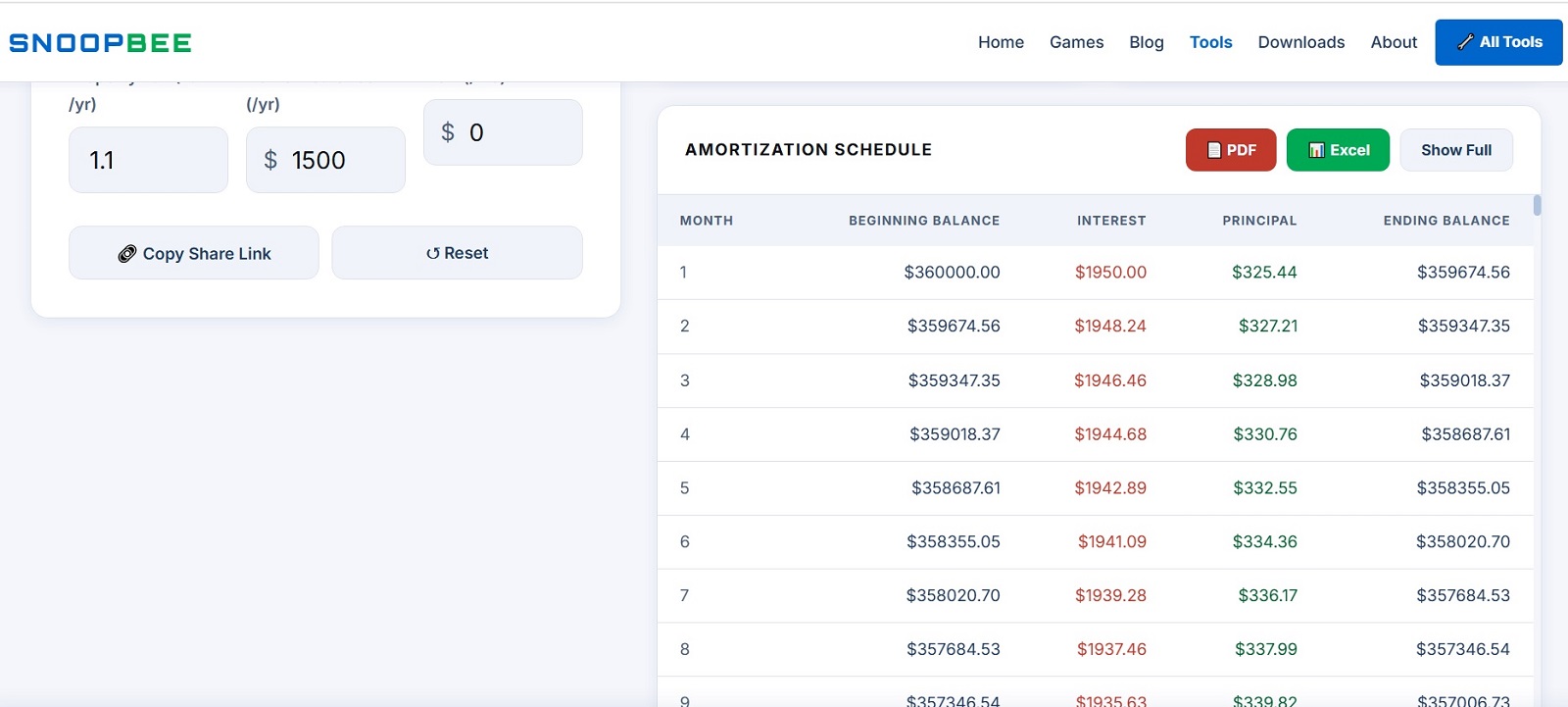

Amortization Schedule Explained

Now that you know the definition, here's what an amortization schedule looks like in practice. It's a complete month-by-month breakdown of every payment for the life of the loan, showing exactly how much goes to interest and how much reduces your balance.

In the early years, the majority of each payment goes to interest, because interest is charged on the full outstanding balance. As the balance shrinks, the interest portion shrinks with it, and the principal portion grows — by the final years, almost the entire payment reduces the balance. This is why home equity builds slowly at first and accelerates later.

Verified Amortization Schedule — $350,000 loan, 6.5%, 30 years (selected months)

| Month | Payment | Interest | Principal | Remaining Balance |

|---|---|---|---|---|

| 1 | $2,212.24 | $1,895.83 | $316.41 | $349,683.59 |

| 120 (Year 10) | $2,212.24 | $1,610.31 | $601.93 | $296,716.43 |

| 240 (Year 20) | $2,212.24 | $1,061.71 | $1,150.53 | $194,828.27 |

| 360 (Year 30) | $2,212.24 | $11.97 | $2,200.27 | $0.00 |

These figures were recalculated directly from the standard amortization formula for this article — you can reproduce them yourself, or generate the complete 360-row schedule (plus a downloadable Excel file) using the calculator.

Extra Principal Payments & Interest Savings

Making extra payments toward principal is one of the most effective ways to cut the total cost of a mortgage. Every additional dollar reduces the balance immediately, which means every future month accrues less interest — the savings compound for the rest of the loan.

Verified examples — same $350,000 loan at 6.5% for 30 years:

| Scenario | New Payoff Time | Time Saved | Total Interest Paid | Interest Saved |

|---|---|---|---|---|

| No extra payment | 30 years | — | $446,406 | — |

| +$100/month | 26 years 6 months | 3 years 6 months | $383,779 | $62,627 |

| +$200/month | 23 years 10 months | 6 years 2 months | $338,309 | $108,097 |

Try it yourself: the Global Mortgage Calculator has an "Extra Monthly Payment" field that recalculates your real payoff time and interest savings live — using your actual loan amount and rate, not a generic example.

Bi-Weekly Payments Strategy

Instead of one monthly payment, pay half your monthly payment every two weeks. Because a year has 52 weeks, this produces 26 half-payments — the equivalent of 13 full monthly payments instead of 12. That one extra payment per year goes entirely to principal, and over a 30-year loan this typically shortens the term by roughly 4 to 6 years, depending on your interest rate, while saving a meaningful chunk of total interest. One practical note: confirm with your loan servicer that bi-weekly payments are applied to principal immediately rather than held until a full monthly payment accumulates — some servicers do the latter, which erases most of the benefit.

15-Year vs 30-Year Mortgage Comparison

Verified comparison — same $350,000 loan, same 6.5% rate:

| Feature | 30-Year Loan | 15-Year Loan |

|---|---|---|

| Monthly Payment | $2,212.24 | $3,048.88 (≈38% more) |

| Total Interest Paid | $446,406 | $198,798 (≈56% less) |

| Interest Saved by Choosing 15-Year | $247,608 | |

The 15-year loan costs more per month but saves an enormous amount over the life of the loan. The right choice depends on whether your budget comfortably absorbs the higher payment — a 30-year loan with extra payments offers a middle path, giving you payment flexibility while still letting you accelerate payoff when you can afford to.

Refinancing & Break-Even Points

Refinancing replaces your current loan with a new one, usually to get a lower rate. It isn't automatically a good idea — you need to calculate the break-even point: how many months of savings it takes to recover the closing costs.

Worked example: a $300,000 remaining balance, refinancing from 7% to 5.5% (both on a fresh 30-year term for comparison), with $6,000 in closing costs:

- Old payment at 7%: $1,995.91/month

- New payment at 5.5%: $1,703.37/month

- Monthly savings: $292.54

- Break-even: $6,000 ÷ $292.54 ≈ 20.5 months (about 1 year 8 months)

Caveat: if you refinance back into a fresh 30-year term, you may be extending your total payoff timeline even while lowering your monthly payment — run the total-interest comparison too, not just the monthly savings, before deciding.

Tax Implications of Mortgage Interest

In the United States, mortgage interest can be tax-deductible if you itemize deductions on Schedule A instead of taking the standard deduction. Current law (the Mortgage Interest Deduction) generally allows interest to be deducted on up to $750,000 of acquisition debt for loans originated after December 15, 2017 (the limit is $1 million for older loans, subject to grandfathering rules). State and local tax deductions, including property tax, are capped at $10,000 combined (the "SALT cap") under current federal rules.

Because the standard deduction is now relatively high, many homeowners — especially those with smaller loans or lower interest rates — find that itemizing no longer saves them more than simply taking the standard deduction. Whether the mortgage interest deduction benefits you depends on your total itemizable deductions, your filing status, and your loan size. This is genuinely individual — a qualified tax professional can run the comparison using your actual numbers; this guide can't substitute for that.

FHA vs Conventional vs VA Loans

The mortgage formula is the same regardless of loan type, but the rules around insurance, down payments, and eligibility differ significantly:

| Feature | Conventional | FHA | VA |

|---|---|---|---|

| Minimum Down Payment | As low as 3% | As low as 3.5% | 0% for eligible veterans |

| Mortgage Insurance | PMI, cancels at 78–80% LTV | MIP — usually required for the life of the loan if down payment <10% | None, but an upfront VA funding fee usually applies |

| Credit Score Flexibility | Generally stricter | More flexible, accepts lower scores | Flexible, lender-dependent |

| Who Qualifies | Most borrowers | Most borrowers, popular with first-time buyers | Active military, veterans, some surviving spouses |

The trade-off with FHA loans is important: the lower down payment and easier qualification come with mortgage insurance premium (MIP) that, unlike conventional PMI, often can't be cancelled simply by reaching 80% equity — for many FHA loans it lasts the life of the loan unless you refinance into a conventional loan later. VA loans, available to eligible veterans and service members, are usually the most cost-effective option when you qualify, since they avoid recurring mortgage insurance entirely.

How These Rules Differ Outside the US

Our calculator now supports 10 countries across 6 regions, because the "extra costs" layered on top of principal and interest vary enormously around the world:

- Canada: mortgages compound semi-annually by law. Above 80% LTV, CMHC mortgage default insurance is required — a one-time premium (roughly 2.8%–4.0% of the loan depending on LTV) usually added to the loan principal rather than billed monthly.

- United Kingdom: there's no annual property tax tied to home value, but buyers pay Stamp Duty Land Tax (England/NI) as a one-time charge at completion. On a £500,000 home under current post-April-2025 bands, that's roughly £15,000 — a cost easy to forget when budgeting.

- Ireland: stamp duty runs 1% up to €1m, 2% up to €1.5m, and 6% above that. The annual Local Property Tax is self-assessed and banded, and your local council can adjust it up or down by 15–25%.

- Germany: the one-time Grunderwerbsteuer (transfer tax) ranges 3.5%–6.5% by federal state. There's no PMI-style insurance — instead, banks typically require 20–30% equity (more for non-residents). German mortgages also usually fix the rate for only part of the term (the Zinsbindung, often 10 years), not the whole loan, which our full-term-fixed model simplifies.

- Australia: stamp duty varies significantly by state, and loans above 80% LVR usually require Lenders Mortgage Insurance (LMI), typically a one-time premium of 1%–5% of the loan.

- New Zealand: there's no stamp duty at all — one of the simplest closing-cost pictures in the calculator. Above 80% LVR, banks instead charge a one-time Low Equity Premium, or sometimes an ongoing rate margin instead.

- Brazil: many mortgages (SFH/SFI) use rates linked to an inflation index (TR or IPCA) rather than a flat fixed rate, which our fixed-rate model doesn't capture — treat results there as a simplified baseline.

- India: stamp duty plus registration typically run 5%–8% of the property value depending on the state. There's no PMI-equivalent, but under the old tax regime, principal repayment plus stamp duty qualify for a combined ₹1.5 lakh deduction (Section 80C) and loan interest for a separate ₹2 lakh deduction (Section 24(b)) — neither applies if you've opted into the new tax regime.

- South Africa: Transfer Duty follows a sliding scale set by SARS — zero below R1,210,000, rising to 13% on the portion above R13,310,000 — and applies only to private resale purchases; buying from a VAT-registered developer means paying VAT instead.

Common Mortgage Calculator Mistakes to Avoid

A calculator is only as accurate as the numbers you put into it. These are the most common ways people end up with a misleading result:

- Quoting principal & interest only, and forgetting PITI. A loan officer's advertised payment is frequently P&I only. Always add property tax, insurance, PMI/MIP, and HOA before comparing two offers — the cheaper-looking rate isn't always the cheaper total cost.

- Using a national-average property tax rate instead of your actual local rate. Property tax rates vary enormously by state, county, and even school district — sometimes by 3-4x within the same country. Always use your specific local rate if you know it.

- Forgetting that 15-year and 30-year loans are sometimes offered at different rates. Lenders frequently price 15-year loans slightly lower than 30-year loans (often by 0.25%–0.75%) because the lender's risk window is shorter. Ask your lender for the actual quoted rate on each term rather than assuming they're identical.

- Ignoring one-time costs. Stamp duty, CMHC/LMI premiums, and closing costs aren't part of your monthly payment, but they're real cash you need at or before closing — budget for them separately, as this calculator does.

- Treating an amortization schedule as fixed when your rate is variable. Everything in this guide assumes a fixed rate. If you have an adjustable-rate mortgage (ARM), your schedule will recalculate whenever the rate resets — treat any fixed-rate projection as valid only until your next reset date.

Smart Tips to Save Money

- Aim for at least 20% down to avoid PMI (US) or insurance premiums (Canada/Australia) entirely, if your budget allows.

- Make extra principal payments as early in the loan as possible — the earlier the payment, the more interest it prevents.

- Confirm bi-weekly payments are applied immediately to principal, not held by your servicer.

- Run the numbers on both 15-year and 30-year terms before committing — and consider a 30-year loan with voluntary extra payments as a flexible middle ground.

- Before refinancing, calculate your real break-even point, not just the lower monthly payment.

- Review your full amortization schedule yearly — export it from the calculator to PDF or Excel and track it against your actual statements.

See These Numbers With Your Own Loan

Open the Global Mortgage Calculator →This article is for general educational purposes only and is not financial, tax, or legal advice. Figures are illustrative examples calculated from the standard amortization formula; your actual rate, taxes, insurance, and loan terms will vary. Always confirm numbers with a licensed lender, tax professional, or financial advisor before making a borrowing decision.

💬 Reader Feedback & Questions

Share your own mortgage math, a calculator suggestion, or a question about PITI, amortization, or any of the 10 countries covered. (Max 200 words)